An increasingly complex world is putting supply chains under more pressure than ever before. Can insurers respond with the type of cover that global businessess need?

Events of the past year have provided a graphic demonstration of the risk faced by global supply chains. The Chilean earthquake brought the country’s transport infrastructure to a halt, while the volcanic ash cloud halted flights across Europe. More recently, there was the catastrophic flooding in Australia, which closed a major international port, and now the political unrest in the Middle East could have a significant impact on international trade.

And it is not just high-profile events such as these that can disrupt trade and break supply chains. More prosaic incidents, like a fire at a key supplier, a strike at a port, or an IT failure, can have dramatic implication for a business’s supply chain. And as supply chains become ever more extended and as costs are taken out to improve efficiency, the potential for disruption has increased.

“Supply chain risks are high on risk managers’ agendas. They are hugely aware of this. It is increasingly at the top of their list of exposures,” says Airmic technical director Paul Hopkin.

Assessing the impact

A recent survey by the Business Continuity Institute found that nearly three-quarters of companies experienced at least one supply chain disruption last year, with an average of five disruptions experienced.

The impact of these disruptions can be costly. One in 10 companies put the financial cost of the disruptions at over €500,000, while one in five respondents said the company’s brand or reputation had suffered as a result of third-party failures.

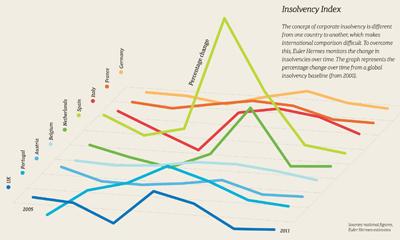

Zurich global supply chain proposition manager Nick Wildgoose says: “During the recession, insolvency [of suppliers] has been an issue for supply chains. And although the rate of insolvencies is dropping, it continues to be a risk as companies expand and pressure is put on cashflows.

Changes in corporate insolvency 2005-11

Wildgoose adds: “A bigger concern is political risks, such as what is happening in the Middle East. The breadth of exposures is considerable. Supply chains are more global in nature and therefore more sensitive to disruption.”

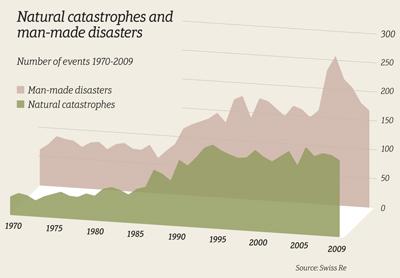

Technology group Invensys vice-president of risk management and insurance Chris McGloin says: “The disruption arising from natural catastrophes has always been an issue for supply chains. What has changed is that people expect things to happen quickly, so if there is a disruption, it will have a significant impact. You need to focus on the interdependencies.”

Catastrophe events 1970-2009

It is not surprising that brokers and insurers are reporting a growing interest in trade disruption insurance cover to protect their supply chains. Rupert Sawyer, a supply chain specialist at broker Miller, says the number of enquiries relating to supply chain insurance has increased significantly this year.

“In the past few years, there has been demand from sophisticated buyers to protect supply chains and business revenues. High-profile natural catastrophes and political unrest have raised interest and increased demand,” he says.

Sawyer says the number of enquiries for supply chain interruption cover has risen by 20%-30% over the last 12 months, following a 20% increase the year before. The number purchasing insurance has also increased, rising by around 10% over the past year.

Covering all eventualities

While interest in the supply chain insurance is increasing, risk managers say the insurance market is struggling to provide a comprehensive response to supply chain risk.

Traditionally, insurers have focused on business interruption arising from property damage, but they have struggled to provide cover where the disruption arises from an event in which there is no physical damage, such as a strike at a port.

Miller and Lloyd’s insurer Kiln developed a trade disruption policy over 20 years ago, which broke the link with physical loss or damage, providing cover on a ‘named perils’ basis.

Since then, a few other insurers have entered the market, most recently Zurich, which launched a product in 2009 providing cover on an ‘all risks’ basis as a way to cover non-physical damage business interruption. Yet this class of insurance is still in its infancy and the market is small in size.

Kieron Russell, an underwriter in Kiln’s enterprise risk management group, says that not many companies buy trade disruption insurance. “Not everyone is aware of it and is comfortable enough to purchase it,” he says.

Tom Teixeira, life sciences practice leader in the global markets international division at Willis Group, says: “The key challenges in the carrier community for this type of risk are availability of required capacity and pricing. Various solutions are being discussed and strategies being formulated.”

Getting the solution right

Airmic’s Paul Hopkin says insurers are not offering the breadth of cover that risk managers would like. “Insurers have the ability to respond by offering contractors’ extensions, often linked to insured perils, and they have the desire to respond to non-damage business interruption, but they need a significant amount of information, which is often difficult for the insured to obtain. Pricing the risk and understanding the risk is difficult.”

Chris McGloin at Invensys says a more “joined-up” response from insurers on physical and non-physical damage business interruption is required. “We’ve always looked at supply chain risk, but we have been looking at the insurability part more recently. As a business we take on risk, but we want the insurance market to take on the catastrophe exposure.

“We need a simple product covering a complex situation. There are relatively few insurers that are gearing up to do it.”

Zurich will therefore be hoping that its ‘all risks’ approach will respond to the requirements of risk managers. Meanwhile, Kiln is developing the breadth of cover it can provide, adding elements such as cover for disruptions arising from the failure of IT networks, product recalls and regulatory investigations.

Miller’s Sawyer concludes: “Trade disruption has been an area where insurers have for a long time failed to grasp a rapidly growing need for insurance to match the new virtual supply chains where companies no longer fit the cosy model of traditional, owned, industrial manufacturing.” It’s time for insurers to catch up. SR

What is trade disruption insurance?

Supply chain interruption or trade disruption insurance covers the financial consequences that occur when a company’s supply chain is disrupted and/or interrupted beyond its control.

The disruption may be caused by: political events, such as a trade embargo; a physical event, such as a closure of a port or a strike; a natural peril, such as a windstorm; or a commercial event, such as the insolvency of a key supplier. It differs from traditional business interruption policies, which are linked to physical damage.

Trade disruption insurance is targeted at businesses with an extended supply chain, in particular those employing a ‘just-in-time’ approach to manufacturing, or outsourced production and service functions.

But trade disruption insurance is a complex area, and the market for this type of cover is relatively limited. Risk managers say that it is often difficult to fully describe and document the risks to which the supply chain is exposed, which makes it hard for underwriters to provide appropriate cover and price the risk.