Global financial analysts predict global economic growth of 3.5% and suggest ten economic risks for 2012

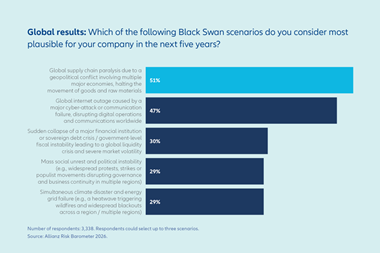

![]()

Investors can expect another turbulent year in 2012 the result of political uncertainty, low growth and low interest rates, according to BofA Merrill Lynch’s Global Outlook.

Against a backdrop of a looming recession in Europe, a still-struggling US economy, high oil prices and slower growth in China, BofA Merrill Lynch forecasted global economic growth of approximately 3.5 % during 2012.

The macro-analysts also anticipated that credit and commodities will outperform equities in the first half of 2012.

“The global economy can weather a normal size recession in Europe, in our opinion,” said Ethan Harris, co-head of Global Economics Research. “The US faces its own challenges, with gradual fiscal tightening and considerable uncertainty around policy after the election. As a result, while we expect solid 3 % GDP growth in the current quarter, we look for growth to slow to just 1 % by the end of 2012.”

Michael Hartnett, chief Global Equity Strategist and chairman of the BofA Merrill Lynch Research Investment Committee (RIC), added: “The very real risk of policy mistakes causing a recession in the U.S. or a hard landing in China means that investors should conservatively allocate assets in 2012. Despite our short-term caution, however, we anticipate that global equities could rally by 10 percent next year from current levels, aided by liquidity, modest earnings growth and cheap valuations. In a bullish scenario, 2012 could represent the beginning of the end of the great bear market in equities.”

“Emerging markets will de-couple from the U.S. and Europe, but the combination of lower growth in developed economies and moderately high commodity prices place emerging economies in a difficult position,” added Alberto Ades, co-head of Global Economics Research and head of GEMs Fixed Income Strategy. “The global growth malaise will mute export activity and temper demand for commodities, creating significant risks for emerging market investors in 2012.”

Ten macro themes for 2012

Slower economic growth. Co-heads of Global Economics Ethan Harris and Alberto Ades forecast that global GDP growth will slow modestly to 3.5 percent in 2012. The U.S. economy will enter 2012 with momentum but weaken in the second half to just 1 percent annualized growth in the fourth quarter of 2012. They expect Europe will see a mild recession, while emerging market economies will see growth of 5-6 percent. Asia should remain the most resilient with growth of 7.1 percent and Latin America should see growth of 3.3 percent.

The US consumer will weaken…again. The U.S. Economics group expects the recent momentum from U.S. consumer spending to subside in coming quarters, absent much stronger jobs creation or wage growth. Consumer de-leveraging will remain a drag on the U.S. economy in 2012.

A soft landing in China. China is vulnerable to a U.S. and European recession, but a healthy balance sheet, slowing inflation and massive foreign reserves mean China can ease aggressively, if necessary. The Global Economics team expects China to avert a hard landing and forecasts GDP growth of 8-9 percent in 2012. As inflation risks fade in 2012, the group looks for Chinese policies to turn increasingly pro-growth.

Quantitative easing in the U.S. and Europe. Tighter fiscal policies in the U.S., Europe and Japan are likely to be offset by accommodative monetary policies around the world, aided by lower inflation. Importantly, the Global Economics team projects fresh rounds of quantitative easing by mid-2012 in both the U.S. and Europe. The RIC expects that this will prove to be an important inflection point for risk assets and could support commodity prices in the second half of 2012.

US Treasuries to remain the safe-haven asset of choice. Head of U.S. Rates Strategy Research Priya Misra expects the Fed to communicate a much longer on-hold policy. She expects 10-year Treasury yields to fall to 1.6 percent early in the year due to risks from Europe, triggering policy response which should help rates increase to 2.4 percent by year end. While Treasuries are likely to remain a safe-haven asset, the downside and upside on yields are expected to be limited.

Yield and income will remain paramount. The year 2012 will likely be another environment of low rates and scarce yield, and investors will continue to seek assets that provide attractive yields. U.S. Credit Strategist Hans Mikkelsen is bullish on corporate credit and expects credit spreads to tighten significantly by the end of 2012. The credit strategy team forecasts total returns of 4.8 percent and 13.9 percent from U.S. investment-grade and high-yield bonds, respectively.

Modest upside for equities. Equities should offer roughly 10 percent upside in 2012. Deleveraging and slower earnings growth are expected to limit the upside, while quantitative easing, valuation and positioning limit the downside. The Global Equities team recommends focusing on sectors that provide high growth, high quality and high yields. The equity strategy teams’ 2012 year-end targets are 330 for MSCI All Country World Index and 1,350 for the S&P 500.

Large-cap equities will outperform small-cap equities. Head of U.S. Small-Cap Strategy Steven DeSanctis expects large caps to continue to outperform small caps in 2012 as earnings growth and valuations are better for larger companies. Heightened volatility and macro uncertainty offset the clean balance sheets and potential for M&A within small caps.

Stock picking opportunities likely to emerge. Correlation and volatility are likely to decline in 2012, once a macro solution for Europe’s debt problems is implemented. This environment favors active fund management in the year ahead.

Emerging market interest rate cuts support risk assets and commodities. Despite risks, the Global Economics team expects emerging markets to continue to be the engine of global growth in 2012. Emerging market government debt-to-GDP ratios are well below those in developed markets, leaving room for increased public spending. And as recent monetary policy easing in Brazil, Russia and Indonesia suggest, emerging market

![Luke Carrivick[48] (2)](https://d9x705hv73pny.cloudfront.net/Pictures/380x253/4/6/0/121460_lukecarrivick482_160635.jpg)

No comments yet